I mean, after all, here is a (wildly) successful speculator turned philanthropist and all around do-gooder who admits in the introduction to the book that he really wants to be know as a philosopher. If you follow these things, you will also know that he has written essentially the same book three times in the last 20 years, each time crying wolf and predicting an end to the "super-bubble" of financial capitalism, and has lately has been ceaselessly flogging his "theory of reflexivity" in the dozens of articles and op-eds his success affords him. And to top it all off, Soros is a quite perfectly atrocious writer, though, of course this is but par for the course in finance; the world's most interesting system as analyzed by bunch of over educated but somehow only semi-literate neanderthals in suits.

In short, you would be forgiven for not taking the book completely seriously, intellectually speaking.

And yet, I think Soros actually has something quietly profound to say. Yes, you have to wade through some 50 pages of what only a very generous reader could describe as "philosophy" (Do we really need repeated explanations of how we both think about the world as well as act in it? Does this come as some sort of new philosophical problem? Does Soros do anything new to help us understand it?). But once you get through this, you realize that Soros has actually outlined, in his own ploddingly schizophrenic manner, a theory of feedback loops that makes a lot of sense, particularly in the context of financial markets.

The basic idea is the relatively simple ones that Keynes (who was admittedly stiff competition, verbally speaking) put much more eloquently -- "successful investing is anticipating the anticipation of others". Soros describes this as the "two way interaction of thinking and reality". Reality, of course, is defined as the actual economic fundamentals at any given moment. Things like how many teddy bears are being manufactured, or how much demand there is for gold. Thinking, by contrast, involves the anticipation of changes in these quantities and the calculation of how they fit together. If lots of people want golden teddy bears and there aren't many of them, their price will increase. The prices of assets in financial markets are in this sense thinking about reality.

Typically, of course, financial market prices and economic fundamentals stay rather closely aligned. Companies who say they are going to make less money next year see their stocks fall, and when guy with a towel on his head can't find reverse on a soviet tank, the price of oil goes up. No mystery here. Neither is it news that prices in financial markets influence the future course of the economic fundamentals they currently reflect. After all, neoclassical economics has touted for a long time that one of the fundamental purposes of a market is as a price signalling mechanism that helps us determine what we need to make more or less of. So Soros is utterly in error when he claims that the idea that prices can interact with fundamentals, and that changes in prices (thinking) can cause changes in fundamentals (reality), is in any way a new idea.

What Soros does contribute, however, is a more general theory about the way prices and fundamentals interact. He calls this his "theory of reflexivity". He simply means that prices and fundamentals are involved in a feedback loop, and that they reciprocally impact one another. As I say, classical economics understands this quite well, but assumes that the feedback loop is always a negative feedback loop, the type of feedback loop you find in control systems such as a thermostat that tend to maintain themselves at equilibrium. Usually this is a pretty good assumption. If I see my neighbor charging a fortune for his new housingdefaultswap.com website, I might be tempted to get in on the act and make one for myself. The high price leads to an increased supply which leads to a low price. The system tends towards equilibrium.

Soros simply points out that this negative feedback loop, where random fluctuations tend to damp themselves out, is really a special case (even if it is the more common one). Sometimes prices and fundamentals interact via a positive feedback loop where higher prices lead to even higher prices, or vice versa. Economics doesn't deal with these situations too much for a very good reason -- they lead inherently in the direction of infinity. Infinity, as usual, is a problem. Some days, I think infinity is the only problem, but that's a story for another post. Anyhow, because of the counter-intuitive idea of prices spiraling upwards (or downwards) in a feedback loop, and the mathematical intractability of any system that works like this, we have tended to ignore this possibility. Which is odd, because there is absolutely overwhelming evidence that it happens all the damn time in the real world.

As a thinking person, you can't work in the financial markets for more than five minutes and still believe that they are perfectly rational efficient equilibrium-tending mechanisms. This idea has always been a farce; what Soros does is describe a simple mechanism by which the markets might tend away from equilibrium. Consider the interaction between the price of a house and how much money you are willing to lend against it. As the value of the house increases, a bank will be willing to lend you more money against this more valuable collateral. If you go out and spend this money on remodeling your house, you will complete a feedback loop where an increase in the price of housing causes the bank to lend more, which causes the price of housing to increase further in a runaway loop.

Stop me if you see where this is going.

There are millions of examples like this, and the point Soros wants to make is that these positive feedback loops live alongside the more common negative ones. In the housing example, the rising prices --> rising debt --> rising prices loop lives alongside the more typical rising price --> increased supply --> lower prices loop. Normally, the (dare we call it ecological?) interaction of these forces leads to a more or less stalbe equilibrium, but this result is not guaranteed in advance, and in some cases, for whatever reason, the positive feedback loop runs out of control and we have what people commonly understand as crashes and bubbles.

Why Soros feels the need to bring up Karl Popper, truth, fallibility and naive enlightenment ideas about scientific progress in this context remains a bit of a mystery to me, but, hey ... everybody should have their day to pontificate in the sun. At any rate, the basic idea is quite simple and really pretty important.

Like most people who think they've said something smart, and like pretty much anyone who considers themselves a philosopher, Soros applies his idea to e-v-e-r-y-thing. Fortunately, I think it's actually a pretty profound idea that you can usefully apply to all kinds of things.

It really is a sort of new paradigm for the financial markets, in contrast to the idea that they are efficient. It gives a (somewhat vague, admittedly) framework for thinking about market mechanisms, and separates out their complexity into two basic types, positive and negative feedback loops. As far as its direct usefulness for succesfully trading ... well, I think you probably have to be George Soros to make money off this idea. After all, he's really just pointing out that momentum trading works under certain circumstances. Once a feedback loop catches on, it will keep going until it blows up, one way or another. You should be able to make money if you identify these mechanisms in the early phase, but its anybody's guess how long a fuse these things have.

I also think his application of the theory to politics is not entirely misguided. Soros is a classic liberal, and was a major critic of the Bush administration. In the book he argues that Bush manipulated the media (our thinking) so that it became completely divorced from reality in the same way that prices and fundamentals get divorced in a financial bubble. Here he shades into philosophy when he should be more careful to talk about mechanism (there are clear feedbacks loops in our political system -- campaing finance and media access and regulation, to cite the simplest ones), but seeing the Bush years as a phenomena similar to a financial bubble is interesting. He refers to this idea as his "super-bubble" theory, and it is part political observation and part analysis of the long credit boom that has occurred since Reagan took office.

Now you can start to think about the structure of a system that is really always out of equilibrium, particularly as you increase the scale at which you consider it; start pondering bubbles within bubbles and other larger-scale phenomena, and you quickly do get into really philosophical territory. After all, the industrial revolution, the evolution of talking monkeys, or the consciousness of an ant colony doesn't sound much at all like a system at equilibrium. "Reflexivity" at this level starts to look like a basic way of restating the theory of immanence (there is no vantage point outside the world) and a stab at perhaps the most fundamental classification of algorithms -- ie. some go on and on, and some stop.

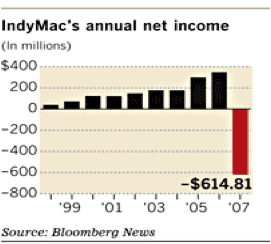

Right so enough already. The last thing is that I found that the book combined well with Nassim Taleb's Black Swan ideas. Taleb would love to beleive that he's being more precise and scientific than Soros the philosopher, but in reality all he points out is that the statistics of the market pretty clearly indicate that it is not efficient because the distribution of outcomes has much fatter tails than you would expect if it were. Fine. But it's not like the guy ever proposes a mechanism for how his alternate Black Swan distribution is actually produced. Maybe you have to pay him $50,000 to eat lunch with you in order to find this out. So while Taleb highlights the off-kilter statistics of a chart like this, Soros actually gives you an idea of what mechanism might have produced those numbers:

No comments:

Post a Comment